7 FAQs about the Washington Divorce Virtual Workshop

The Washington Divorce Workshop is a monthly educational workshop about divorce. The workshop features a family law attorney, financial professional, mortgage specialist, and mental health/wellness practitioner providing professional, reliable information about divorce in Washington state. Here are seven frequently asked questions we get about the workshop.

Four key ingredients for using your divorce to launch into paid work

Most of our stay-at-home parent clients tell us they are terrified about what financial life will look like as a single person. They are pleasantly surprised to learn that they can use their divorce as a launchpad into a new season of paid work.

Don’t overlook the credit report in your divorce

Don’t make any decisions in your divorce without first reviewing your spouse’s credit report. If the credit report includes a lot of late or missed payments, consider whether your spouse can be relied upon to fulfill future financial responsibilities, like making monthly spousal maintenance payments or property buyout payments.

Choosing between the home and retirement

Divorcing individuals must often choose between homeownership and retirement readiness. The ongoing costs of homeownership may impact your ability to save for retirement each month. In addition, keeping the home in the divorce may mean giving up retirement assets.

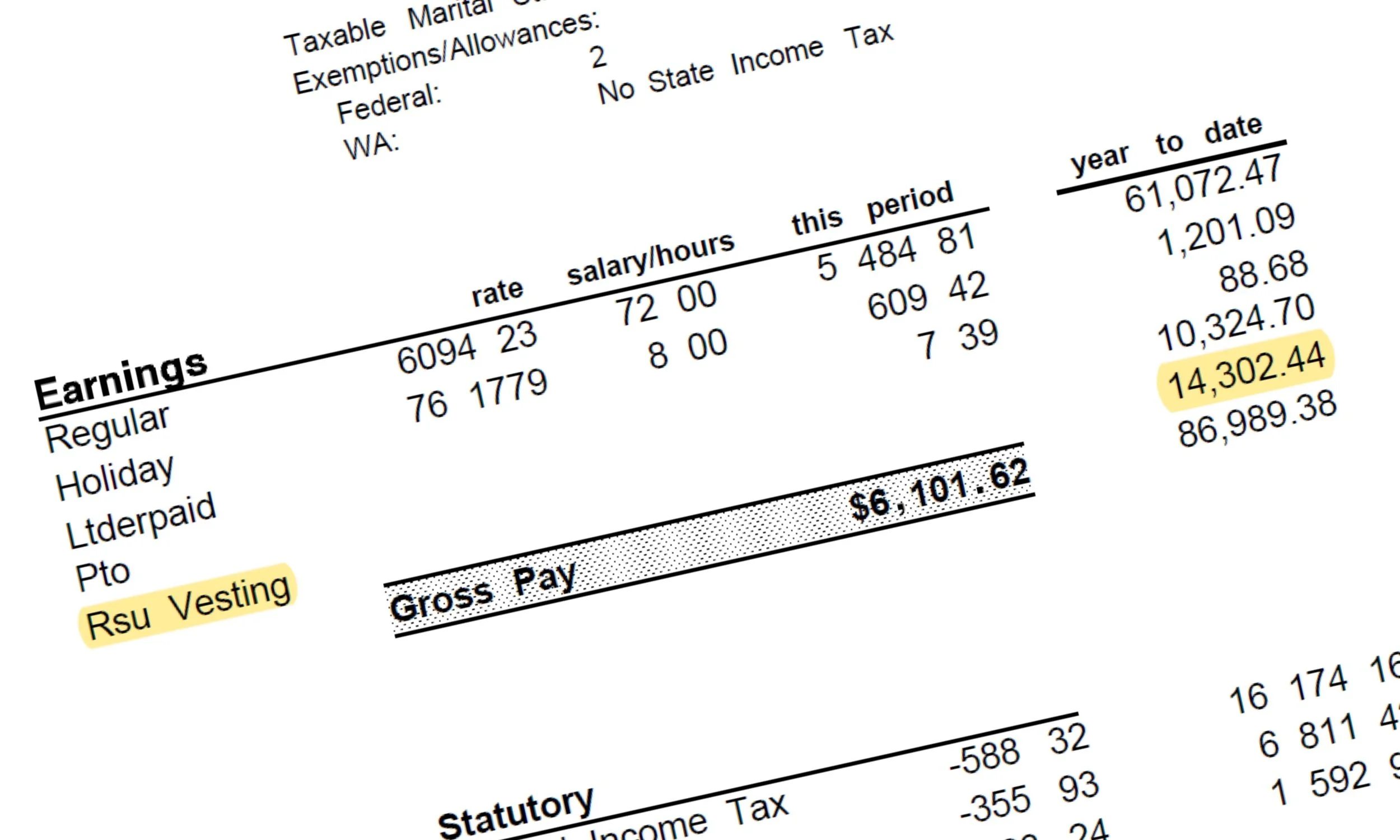

Six FAQs about divorce and RSUs in Washington

Many executive-level employees in Washington state receive restricted stock units (RSUs). RSUs give an employee an interest in company stock. Learn how RSUs are dealt with in divorce and what key documents you can review to find out if your spouse has RSUs.

The Do’s and Don’ts of Building Your List of Assets

Every divorce includes making decisions about dividing up the assets. Before you start negotiating with your spouse about who will get what, take some time to build a comprehensive list of all the assets owned by either you or your spouse. Only when you feel confident that your list includes everything, and that you have an accurate value for each item, should you begin to think about who will keep what. As you begin to build your list, keep in mind these do’s and don’ts.

Two tax rules to know if you are divorcing and keeping the house

Section 121 of the Internal Revenue Code allows some homeowners to reduce the tax owed on the sale of their home. Generally, the rules require that the homeowner has used and owned the home for a certain length of time. Sometimes, divorce results in a situation where the spouse keeping the home is seemingly unable to meet these requirements. Fortunately, there are two special rules for divorced homeowners.

Don’t Make this $10,000+ Tax Mistake in Your Divorce

Savvy taxpayers know they can use Section 121 of the Internal Revenue Code to reduce the tax owned when they sell their home. If you are divorcing, don’t keep the house without first estimating what your tax bill will be if you sell the house as a single person.

Considering a Collaborative divorce? Three questions to ask yourself.

Collaborative divorce may be good option for couples hoping to maintain a positive relationship after the divorce, who have the financial resources to pay for multiple divorce professionals, and who are willing to negotiate the divorce in good faith.

Avoid these 6 mistakes in your post-divorce spending plan

Have no idea what it will cost to live as a single person? Try building a post-divorce monthly spending plan. As you estimate expenses, be sure to avoid these six common mistakes.

Dealing with credit card debt during divorce

Beware assigning your ex-spouse the responsibility of paying off joint credit card debt. If they fail to make the payments, you will be on the hook with the credit card companies. Minimize exposure to your ex-spouse’s financial misdeeds by taking responsibility for paying off joint credit card debt or ensuring that all joint credit card debt gets repaid before your divorce is settled.

I’m divorcing: Can I afford to keep the home?

Thinking about keeping the home in your divorce? Make sure you can afford the mortgage along with your other monthly expenses. Don’t forget to include the costs of routine maintenance, large one-off expenses, and the expense of hiring someone to do the chores your ex-spouse used to do.